The Magnificent 7 Are the New Nifty 50

The Magnificent 7 Are the New Nifty 50

"History doesn't repeat itself, but it often rhymes" — Mark Twain

There have been many comparisons between the current stock market and the dot com bubble from the late 90s. But there are many differences. The main one is that the bubble from the 90s formed around speculative stocks that made no profits. It was all smoke and mirrors.

That’s not the case today. The Magnificent 7 are expensive, but they are great companies. They have solid business models, established positions in their markets, and make obscene amounts of money. Does that mean they can’t be overvalued?

I don’t think so.

The Nifty 50

In the late 1960s and early 1970s, the Nifty Fifty were stock market darlings comprised of a set of roughly 50 large companies. Investing in these firms was not considered speculative, unlike many of the tech firms that dominated the headlines in the late 1990s. Instead, the Nifty Fifty were quite successful, with strong earnings growth and profitability.

— Andrew L. Berkin, from Bridgeway Capital Management

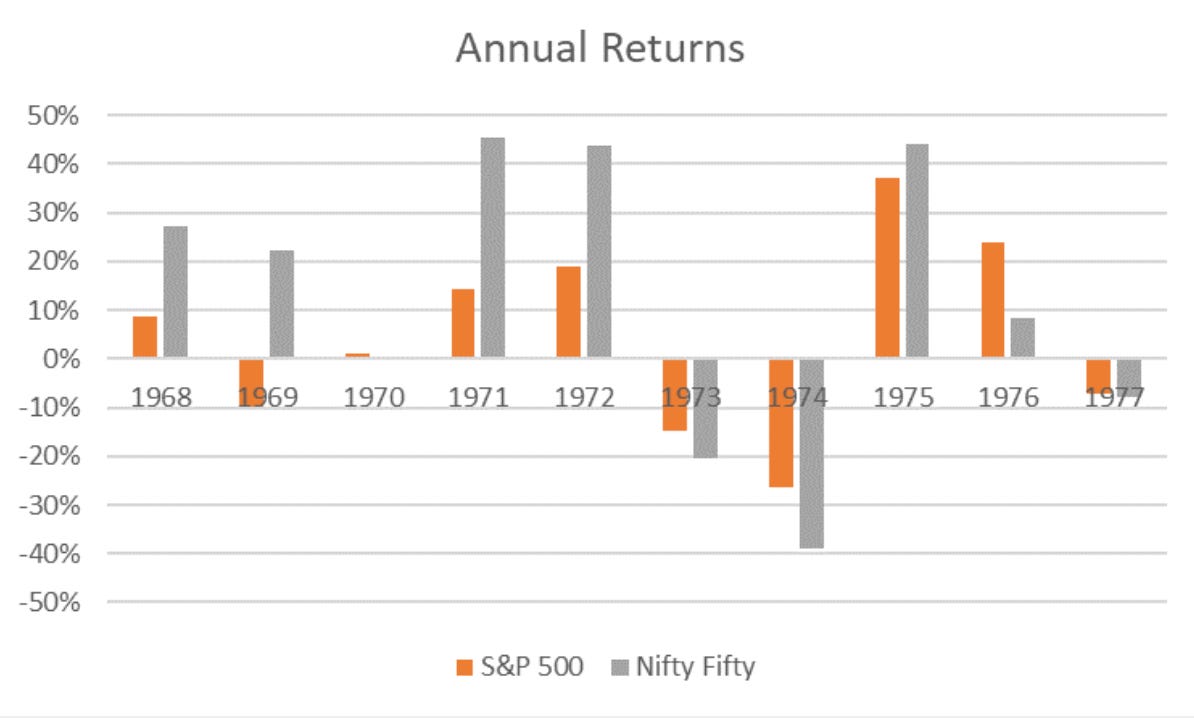

Everyone wanted to own the Nifty Fifty. They traded at an average P/E of 50 in the early 70s. So-called ‘experts’ advised investors to buy them, no matter the price. Most of these companies were already established businesses. Today they are well-known enterprises, such as Coca-cola, IBM, or Walmart.

In the late 60s, they started to outperform the market by a lot, soaring much like the Magnificent 7 nowadays. However, in 1973, things changed.

The bear market of 1973-1974 hit the Nifty Fifty much harder than the rest of the market. Some of these companies took a decade to recover the losses. Johnson & Johnson took the longest: 15 years to make up for the bloodbath.

All of this sounds eerily similar to what’s going on today. The Magnificent 7 are profitable, innovative companies. They’re not meme stocks or SPACs. AI is changing the game. But human psychology remains the same.

Reversion to the mean

The Nifty Fifty were outliers for many years. But outliers can only be outliers for so long. In statistics, a random variable that is outside of the norm will tend to converge closer to the mean. This concept is known as reversion to the mean and most people don’t understand it.

When we see a stock reverting to the mean, we try to find causes. Has the management team changed? Demand dropped? A lawsuit going on? Little do we know that stocks don’t need any reason to revert to the mean. When an athlete wins 5 gold medals in one year, it’s likely she won’t win as many medals next years. Not because her performance is worse, but because winning 5 medals in one year is extremely unlikely.

Mean reversion doesn’t happen overnight though. A hot stock can outperform the market for many years before it reverts back to the mean. So if it’s extremely overvalued, it doesn’t mean it’s going to crash soon.

Photo of the week

Last Sunday I visited this hidden gem — considered the best beach in Europe in 2017.

But that would mean that the people who trade stocks for a living are winning as much by luck as skill. Please don't tell them that! Their egos may never recover!